Having familiarity with some basic real estate terms benefits people that want to buy or sell a home. Uncertainty about rights, duties, obligations, and contracts can lead to expensive mistakes that can be avoided.

Very few people, however, want to read books like The American Bar Association’s Glossary of Real Estate Terms, Fidelity National Title Group’s Real Estate Dictionary, or Old Republic Title’s Real Estate Dictionary. This is understandable. The amount of information there is overwhelming. And not all of it is necessary if you’re only interested in buying or selling a home. Because of this, we’ve decided to compile a list of fifteen core concepts we feel would most benefit the average person engaging for the first time in a real estate transaction. You won’t be a real estate law specialist after reading this, neither will you be a novice.

What is Real Estate Law?

Real estate law is related to every legal issue linked to the possession or inhabitation of land. Building codes, deeds, leases, zoning ordinances, foreclosures, and rental contracts are just some of the issues real estate law covers. Building trusts for the management of commercial property and crafting financial instruments in order develop residential property also fall under the heading of real estate law. The role of real estate attorneys is to help clients achieve their goals, ensure their clients’ rights are protected and provide strategic advice.

Concepts Your Real Estate Attorney Wants You to Know

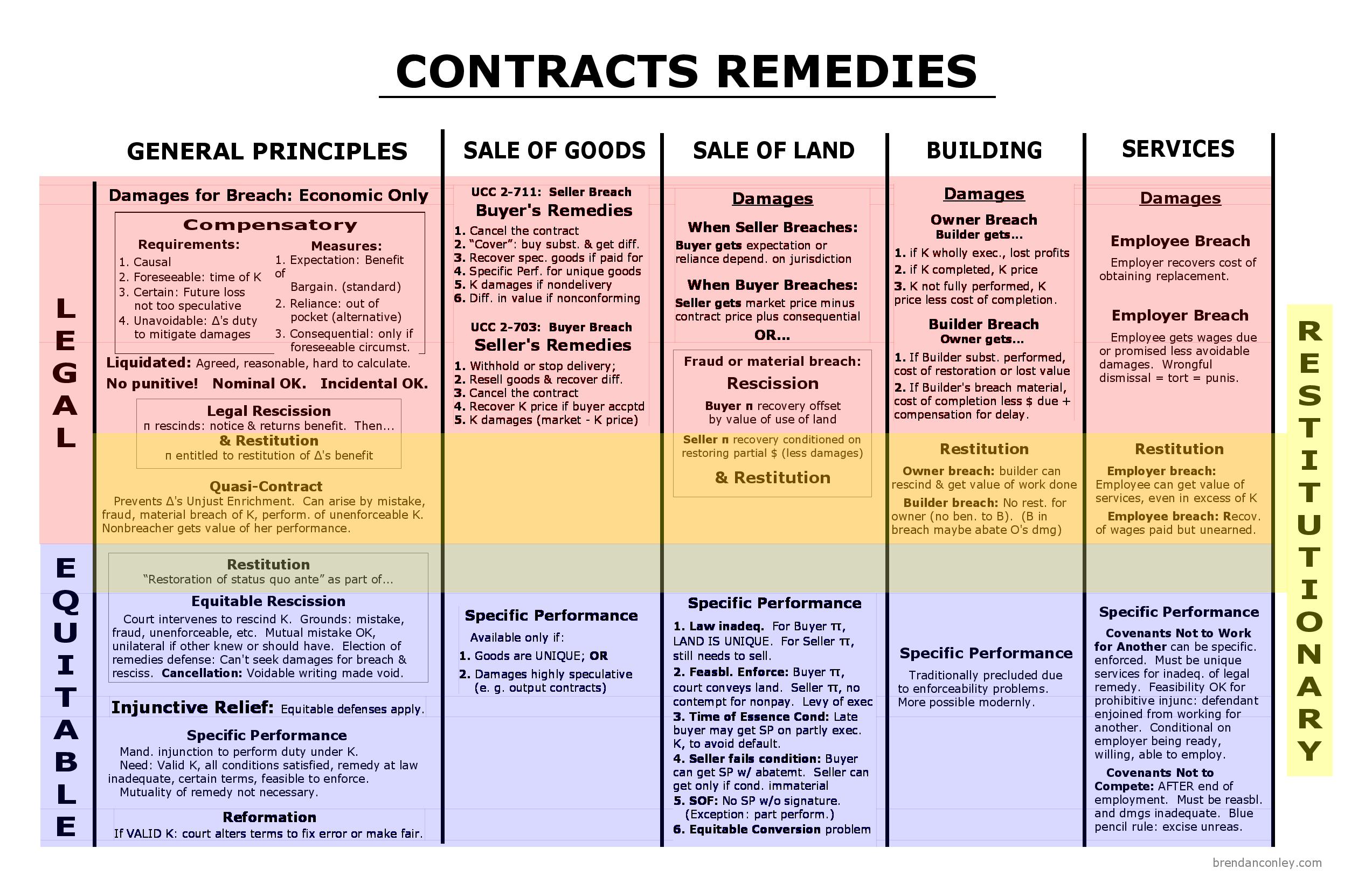

Buyer or Seller’s Default

Source: Brenda Conley

When a buyer defaults, they have not complied with the agreement described in their contract. Judges can issue an order to a buyer to complete the closing on a home. This is an alternative to collecting monetary damages. It is an equitable remedy claim pursued through litigation.

Some examples of buyer being in default includes:

- not sending the initial good faith deposit into escrow on schedule

- cancelling the sale after all contingencies have been cured

- cancelling the sale without cause allowed by the contract

- not fulfilling contingency requirements on time

- ignoring other agreed-to deadlines

- not completing loan paperwork according to the schedule

- not submitting the signed disclosures according to the schedule

- not bringing “good funds” to escrow in time for closing

- no financing contingency was agreed to and the financing falls through

- not purchasing insurance

- failing to show up at the settlement with the required documents

A seller’s default means that “the Seller breached its representations, warranties, covenants, or agreements under this Agreement, or failed or is unable to consummate the sale of the Property by the Closing Date.” In these instances, the buyer has the option to sue for specific performance.

Some examples of a seller being in default includes:

- not completing contractually required work (i.e. home inspection repairs or pest control)

- not keeping the utilities on for inspectors and final walkthrough

- not providing to the title company required documentation, such as loan payoff information

- not providing completed disclosures or reports according to schedule

- refusing to sign the closing papers according to schedule

- not moving out according to schedule

Effective Date

In real estate contracts, the effective date is the date when the buyer and seller have signed or initialed and delivered the offer or final counter offer to the other party. After all parties have come to an agreement and signed the contract, the transaction becomes binding between the parties. Four standards must be met to have final acceptance. These are as follows:

- The final contract must be in a written format. Any oral agreements or modifications will not be considered binding or enforceable.

- Both buyer and seller must sign the contract. Any handwritten changes to the offer must be signed or initialed.

- Acceptance must follow the mirror image rule, i.e. the offer must be accepted as is without modifications; it must be unequivocal.

- The last party to accept the conditions of the contract must communicate acceptance back to either the other party or the other party’s agent.

The effective date of the contract is when the last of all four conditions – communicating acceptance to the other party – is fulfilled. The timelines for performance under the contract begin following the final step. If there is an offer with no acceptance, then no contract is formed.

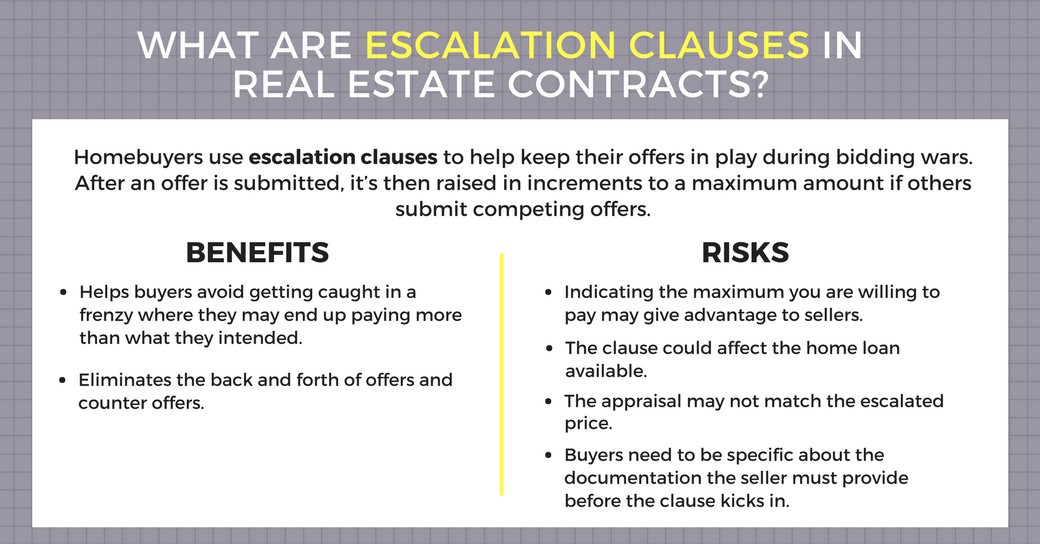

Escalation clause

Source: Blazing Social

An escalation clause is written into purchase offers. It contains language that will automatically increase the purchase price of an offer by a certain amount upon receipt of written, competing bona fide, offers. This number will include a maximum price willing to be paid for the home. If there are no competing offers, an escalation clause will not be triggered.

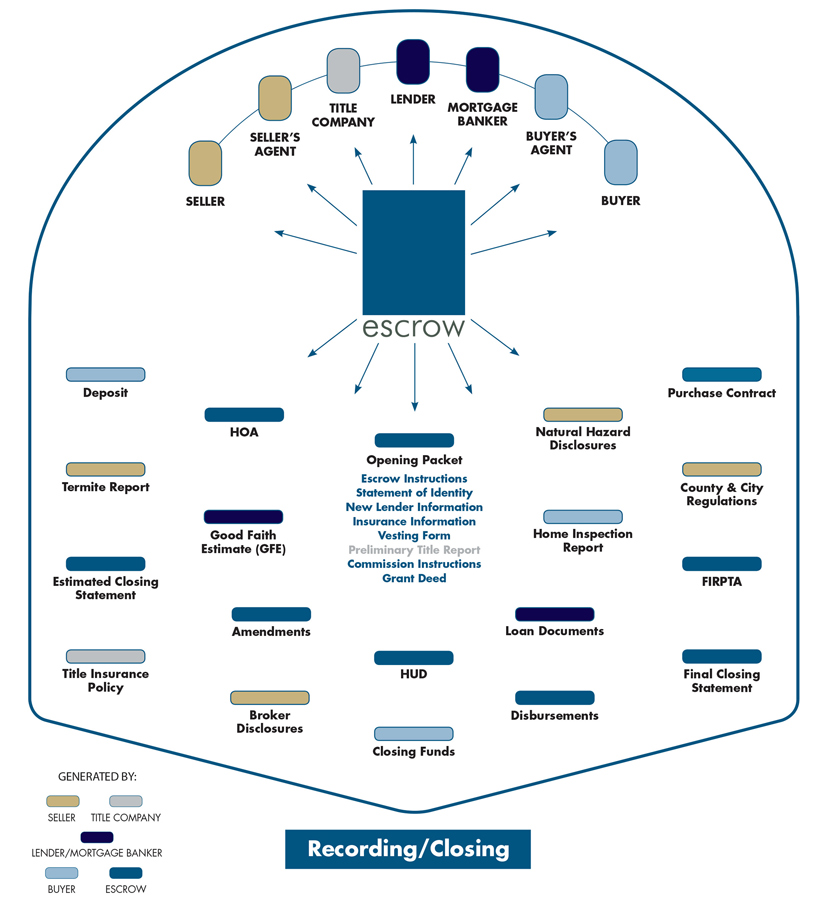

Escrow Agent

Source: Icon Escrow

An escrow agent is a person or entity, not the buyer or seller, but a third party which retains possession of the house and the payments for the house before they are transferred from one party to another. This role is that of a neutral intermediary.

Escrow agents hold funds and the asset until the fulfillment of all contractual obligations under the contract. This arrangement reduces financial risk on both sides. Because of the large sums of money involved escrow agents are frequently associated with real estate purchases and sales. They can, however, be used in any transactional situation where high-value goods – be it physically large items like homes and cars, or even small ones like diamonds.

Financing Contingency

Source:

According to The Washington Post writer Harvey S. Jacobs, The Most Misunderstood Clause in Real Estate Contracts is the Financing Contingency. These contingencies provide risk protection to the buyer.

If a buyer doesn’t yet have financing, but wants to make an offer, it enables the buyer to put money down and have time to obtain a loan. Because the contract for sale is made conditional on the buyer’s loan approval, if the buyer can’t obtain a loan, they are no longer obligated to purchase the property. Under the terms of the contract, they may reclaim their deposit – so long as they do not pass the specified time period agreed to between the buyer and seller.

Should the buyer not terminate the contract due to their inability to get a loan before a certain time, they then become obligated to purchase the house even if no loan has been secured.

While the February 2018 Florida Realtor’s Contract for Residential Sale and Purchase Preparation Manual includes language on financing contingencies, it’s unlawful for Realtors to give legal advice about the various issues which arise in the case of breach of contract.

FIRPTA – Foreign Investment Real Property Tax Act

Image source: Florida Bar

Because Florida is such a popular destination for foreign investment into real estate, having to navigate the Foreign Investment Real Property Tax Act (FIRPTA) is fairly common. Being able to understand all of the activities and implications described in the above chart, that’s not common. The type of person most suited to interpreting this is an attorney that specializes in real estate law.

FIRPTA doesn’t apply if an American citizen purchases real estate from another American citizen. If you are purchasing from a non-citizen or selling as a non-citizen – it does.

According to the Internal Revenue Service, FIRPTA withholdings are a form of income tax withholding. It imposes a tax on capital gains derived by foreign persons from the disposition of U.S. real property interests. Depending on their specific case – foreign persons must pay a 10% or 15% tax when they sell U.S. real estate they own. Withholding of these funds is required at the time of sale, and the payment must be remitted to the IRS within 20 days following closing.

The exemptions, tax amounts, and reporting requirements mandated by the IRS all depend on factors outlined in Withholding of Tax on Dispositions of United States Real Property Interests on the IRS website, detailed further in Publication 515 (2021), and Statue 96-499. Should you want to buy real estate from a foreign national, or you’re a foreign national that wants to sell real estate to ensure your compliance with FIRPTA, you should contact a lawyer for assistance.

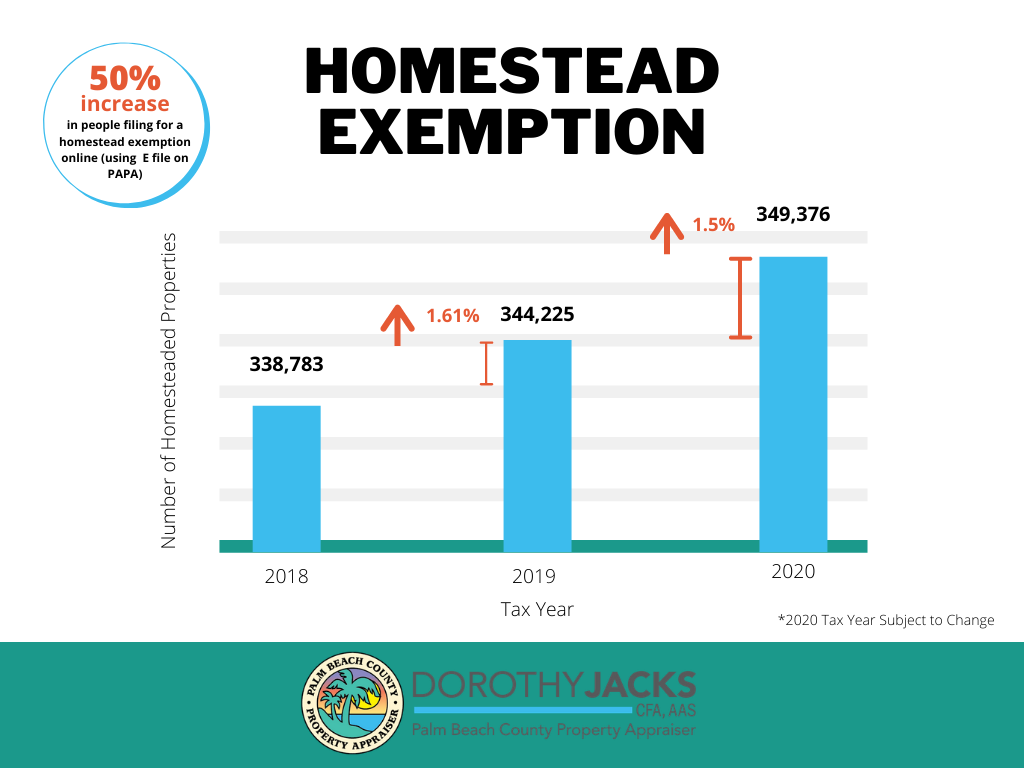

Homestead Exemption

Source: Palm Beach County Property Appraiser Dorothy Jacks, CFA

Homestead taxes are a subject covered in Chapter 196 of Florida Statues. The law on homestead tax in Florida enables property owners who meet specific qualifications to have their annual financial obligations on the assessed value of their property discounted or waived. If you qualify for a homestead exemption of $50,000 and your home is valued at $550,000, then you will only pay property tax on $500,000. There are multiple types of homestead exemptions – including exemptions for people that are disabled veterans, seniors that have a limited income, or people that have certain disabilities.

Homestead exemptions are not permanent. You must file to obtain an exemption every year and there are conditions which, if not met, lead to ineligibility and significant penalties for mistakenly filing an exemption when the exemption no longer qualifies.

For details on homestead tax exemptions, the county property appraiser or tax assessor will have the most up-to-date information on their website. When visiting these websites you can learn information such as the millage rate and tax roll information for Palm Beach County or the millage rate for Broward County. With the knowledge there, you can determine your projected annual property taxes.

Inspection contingency

Source: Coldwell Banker

Inspection contingencies protect buyers. An inspection contingency gives the buyer the right to have the home inspected within a specified period, typically five to seven days.

Also called a “due diligence contingency”, these agreements empower the buyer to negotiate repairs based on the findings of a professional home inspector or cancel the contract.

After an inspector examines the property, they provide a report to the buyer. This document describes the issues discovered during the inspection. Depending on the terms of the inspection contingency agreed to by buyer and seller and the information contained in the report, the buyer can:

- Approve that the deal moves forward.

- Back out of the transaction and have the earnest money returned.

- Request time for further inspections.

- Request repairs or a concession. In such cases, there are two options going forward. The seller refuses, and the buyer can back out of the deal and have their earnest money returned. The seller agrees, and the deal moves forward.

Sometimes included in addition to the inspection contingency is a cost-of-repair contingency.

The best way to learn about all the contingencies that can be used to hedge risk is to hire a lawyer to represent you.

Liens

Source: Levelset

According to 11 USC §101(37) — “lien” means a “charge against or interest in the property to secure payment of a debt or performance of an obligation.” There are a wide variety of liens. Since real estate legal terms are the subject of this article, all of the information shared about liens refer only to property liens.

A lien is, essentially, when a lender or creditor acquires an interest in some type of collateral such as real property. Liens are attached to the physical property, or a part of it, instead of the property owner. Because of this, when a purchaser acquires a home they may unwittingly purchase a financial obligation along with the physical property. Since a seller must convey clear and marketable title, all liens against the property must be satisfied by the seller prior to closing. Examples of liens include, but are not limited to, existing mortgages, unpaid HOA assessments, unpaid IRS tax responsibilities, and PACE financing agreement.

Property Inspection

Problems that can cost tens of thousands of dollars of repairs aren’t always visible to the naked eye, nor to someone not professionally trained. By deploying licensed professionals to inspect the property, current problems or those that will soon worsen may be identified. Contingencies can’t always be used in negotiations, but they can always be used as cause for you to walk away from the purchase contract. If paying for an inspection prior to purchasing the house seems wasteful, consider this counterfactual: How would you feel about purchasing a $450,000 house and then finding out that it needed another $80,000 in repairs that you hadn’t been budgeted? Property inspections, though not always required to obtain a loan, are often worth the investment.

Types of inspections include:

- Four Point: Evaluation of the electrical panels and wiring, the heating, ventilation, and air conditioning (HVAC) systems, the plumbing fixtures and connections, and the roof.

- Wood Destroying Organisms: Examines the property for evidence of termites and other pests that could damage the property.

- Mold: Common in Florida due to the humidity. Free tip: Chances are that if you see mold, you have mold.

- Lead Paint: Many homes built before 1978 used lead-based paint, which generated lead-based paint chips. Checking for this is important, especially if young children will be living in the home.

- Radon Gas: The EPA estimates that radon causes more cancer deaths per year than people that die from drunk driving. Since nearly one out of every 15 homes in the U.S. is estimated to hace an elevated radon level, it should be tested for prior to closing.

If you’re planning on selling your home soon, check out these 10 Tips To Prepare For Your Property Inspection.

Right to Cancel

The right to cancel also called the right of rescission, allows a borrower to cancel a home equity loan or line of credit with a new lender, or to cancel a refinance transaction done with another lender other than the current mortgagee, within three days of closing on a no-questions-asked basis.

According to the Consumer Financial Protection Agency, the clock on this three day period does not start until all of the following three events have occurred:

- You sign the Promissory Note (also known as the credit contract)

- You receive a Truth in Lending disclosure

- You receive two copies of a notice explaining your right to rescind

When this right is exercised, the lender gives up any claim to the property and must refund all fees incurred within 20 days. The right of rescission applies only to the refinancing of a mortgage. It does not apply to the purchase of a new home. If a borrower wants to cancel a loan, they must do so no later than midnight of the third day following the completion of the refinancing.

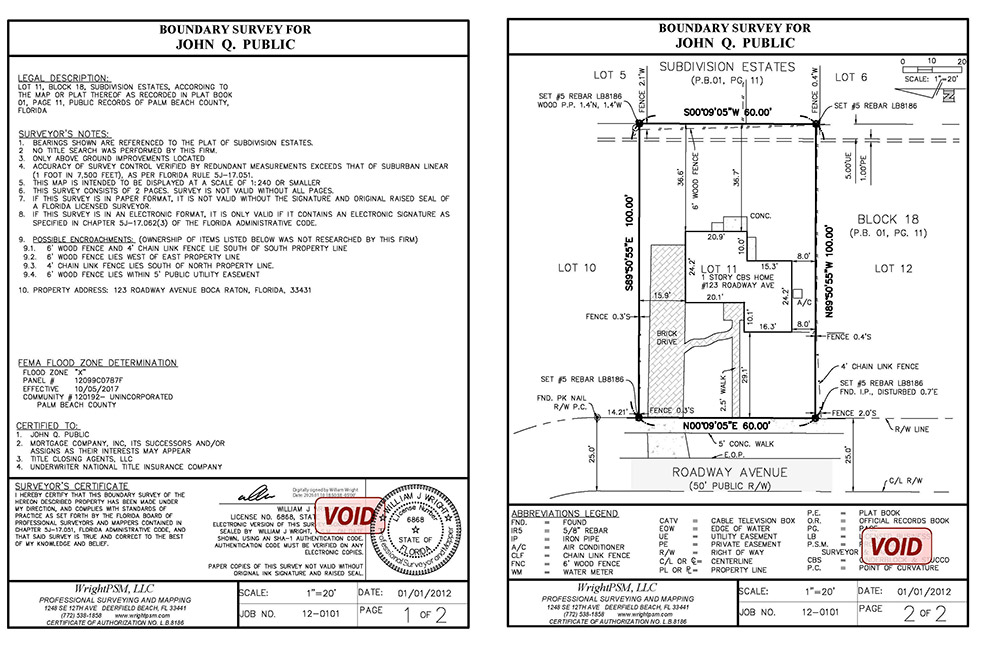

Survey

Source: Wright PSM

A property survey, sometimes called a boundary survey, is used to confirm property lines within the plot of land a home is built on and to describe all of its features. It is a precise measurement produced by professionals. Property surveys are important for knowing property lines or building additions to your home. This knowledge can help you avoid any restrictions or conditions that would interfere with the legal boundaries of the property. The State of Florida does not require surveys to be completed to close the purchase of a home. Your title insurance company, however, will require it. Even if you’re paying for a home in cash, knowing the property’s proper boundaries can benefit you in several ways.

For one, there can be discrepancies that exist between recorded instruments and physical property, topographic charting can indicate unexpected issues, and provide a guide for setback requirement – a restrictive covenant in Florida law the prohibits certain uses of the property.

Then there is the issue of encroachments. Encroachments can raise title insurance costs, lower a property’s resale value, cause liability issues if someone is injured due to the use of a structure, amongst other issues. Encroachment is when someone else besides the owner begins to use your property. An encroachment could be minor – such as the planting of shrubs or trees that grows beyond their property lines. Or an encroachment could be major – a neighbor renovated their garage and part of it is now on your property. Then there’s structural encroachment, such as when as the installation of a shed on your property.

Without a property survey such issues can’t be identified and addressed.

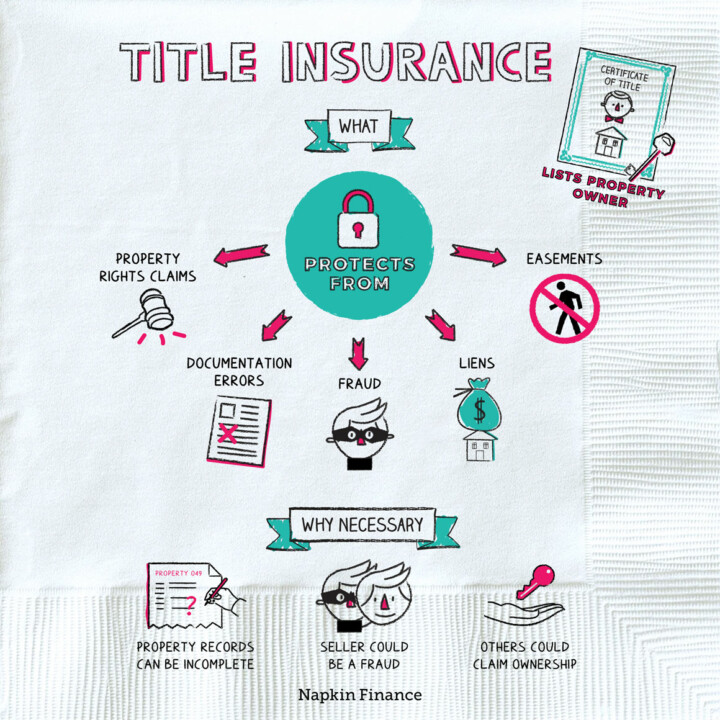

Title Insurance

Source: NapkinFinance

While a title search will inform you of potential trouble sources known in advance, title insurance policies protect your real estate transaction from the unknown. Some of the issues that might come up include:

False impersonation of the true owner of the property

Forged Deeds, releases or wills.

- Perhaps the person you bought the house from was an expert forger, none of the documents they provided you with were genuine, and they didn’t actually own the property.

Undisclosed or missing heirs.

- Perhaps the long-lost nephew of the previous owner returns with paperwork showing that he had been left the property in a will 20 years ago and now wanted to take possession.

Instruments executed under invalid or expired power of attorney.

Mistakes in recording legal documents.

- Perhaps the local office of legal records had an error on the deed or the deed was previously forged.

Misinterpretation of wills.

Deeds by persons of unsound mind.

Deeds by minors.

Deeps by persons supposedly single, but are in fact married.

Liens for unpaid estate, inheritance, income or gift tax.

- Perhaps the previous owner decided to use the home as collateral for a loan the day before closing and decided not to disclose this to the buyer.

Fraud

- Perhaps the previous owner made a conservation agreement with the local government to not develop the property alongside the canal system in exchange for a tax benefit.

- Perhaps a nature trail passes through your back yard and local outdoor clubs had previously been given the right to cross the property which were not disclosed.

In the above-described situations and those like it, title insurance helps pay for the costs to legally resolve these issues.

Title Search

Mortgage records in canvas binders from a government records center

To ensure that the person representing themselves as the property owner is indeed the person with legal ownership and to determine if there are any claims, liens, or judgments on the property, it’s necessary to complete a title search.

When performing a title search, according to Investopedia, a real estate attorney: “conducts research using public records and legal documents to identify the vested owner, liens or judgments on the property, loans on the property, and property taxes that may be due. While it is possible for a prospective buyer or another individual to conduct a title search on their own, it is not generally recommended. Legal documents can be confusing, and gaining access to courthouse records is a difficult process.”

Time

Source: 9th Edition by Roger LeRoy Miller

Time’s legal meaning is different from the common usage of the term. In contract law, the effective date indicates the beginning of mutual, binding obligations. The contract will typically describe guidelines for time periods by which notifications must be made or responses provided. If you are a day late, you can be defaulted under the contract and lose your deposit or be sued for thousands of dollars in damages.

Terms like “ten days” should be specified as business days or calendar days. While “reasonable time” is widely accepted by attorneys to mean 30 days, this isn’t always so when time is of the essence. For a judge, the facts and circumstances of the particular case can determine a reasonable time for performance. A delay in painting the exterior, for example. It’s not a big deal if 20 days have passed and this still hasn’t been done. If a biohazard clean-up is required and the same time has gone by, it’s likely that the judge will metaphorically lob law bombs at the person not being diligent in their agreed-to duties. To ensure that buyers or sellers are informed of their duties and thus aware of the risks they take in delaying action, they ought to hire a real estate lawyer.

Where is Real Estate Law Practiced?

Knowing the terms and being able to successfully deploy them are very different. While dramatic legal procedural television shows give the impression that lawyers are often in court or getting ready to go to court, this is not the case with real estate law. Most of the time real estate attorneys are practicing their profession in law offices and meeting rooms or on the phone. Conflicts between parties in real estate tend to be less adversarial than other legal practices as all know the costs of going to court. But sometimes that’s what is required, and when that’s the case, real estate attorneys go to have their cases heard by a judge.

REALTORS® use a common set of forms and contracts developed by their state-level associations. Because of this, it might seem that real estate attorneys are an unnecessary expense. A wider view of the facts tells a different story, one that gives proof to the adage that: “A little knowledge is a dangerous thing.”

In April October Research, a business publishing company that specializes in the law and real estate, published Attorney State Breakdown: Special Report. They share the facts of over a dozen case rulings and histories in over a dozen states where Legislation either requires real estate attorneys to be involved in transactions by law or do so via custom and practice. The main takeaway there? Put simply: Realtors, title agents, notaries, and other real estate professionals aren’t lawyers. They are more familiar than the average person with the terms, principles, and procedures of real estate law. Nevertheless, the barriers to entry in those professions aren’t as high as those required to practice law and the consequences linked to professional malpractice aren’t as serious.

Requirements to get a real estate license vary by state. Some state-level regulatory agencies mandate that Realtors have a high school diploma while others do not. The other standard for becoming a real estate agent are courses that can be completed in four to six months. Contrast that low barrier to entry with the legal profession. According to the Bureau of Labor Statistics lawyers are required to have successfully completed at least seven years of study – four years of college plus three years of law school a – to practice their profession. To specialize in a practice area, law firms will often require attorneys to obtain additional training in that field.

Inman, the real estate industry’s leading source of information, gives insight into the ways that non-lawyers can end up negatively impacting transactions in their article 10 ways agents typically get slapped with lawsuits. Breach of Duty to the client, false representation of knowledge, misleading clients, and breach of contract are just some of the lawsuits brought against Realtors. While a few instances of this happening shouldn’t be a reason for you to avoid working with Realtors, it’s worth contrasting the professional ramifications of such behavior. Should a realtor be found to be in gross violation of the National Association of REALTORs® Code of Ethics, the worst consequence is being suspended from working as a Realtor for three years. Contrast this with the Florida Bar Disciplinary Review Committee. If they conclude a lawyer engaged in a gross violation of their ethical code, they can disbar that attorney from practicing law for five years and require them to undergo a new character and fitness review before being considered for readmission.

Klein Law Group: Your Real Estate Attorneys for Palm Beach County

Unless you have experience being a real estate paralegal, a realtor, or work experience at a title insurance office or at a bank that originates mortgages, you are not likely to be familiar with the terms we’ve defined here. While familiarity is good, mastery of the subject is better.

It doesn’t matter if you’re looking to buy or sell commercial or residential real estate in Boca Raton, Delray Beach or Palm Beach Gardens. If you’ve been searching online for Palm Beach County Real Estate Lawyers, there’s no reason to look further. Klein Law Group shows up on the first page of Avvo’s Florida Real Estate Lawyers because for more than twenty-five years we’ve been working to ensure our client’s needs are met and that they have a high rate of customer satisfaction with our service. Let us help you achieve your goals by contacting us today.